会员

会员 下载APP

下载APP

Key Takeaways

February's broad credit edged down 10bps YoY, to 8.3%, as the market expected.

owing to LNY disruption of government bond issuance.

But infrastructure support likely accelerated, evident in faster disbursement of

fiscal deposits vs. 2025 and sequentially stronger long-term corporate loans.

Sequential M1 growth also rebounded, a reflection of faster fiscal deposit

drawdown and continued housenold deposit migration towards capital markets.

This echoes our view of infrastructure front-loading despite a flat initial fiscal

package announced at the NPC, anchoring 1Q GDP growth at ~4.8%Y.

But the momentum is unlikely to be sustained, given persistent consumption and

housing weakness, and looming risk to global demand should oil shock be prolonged.

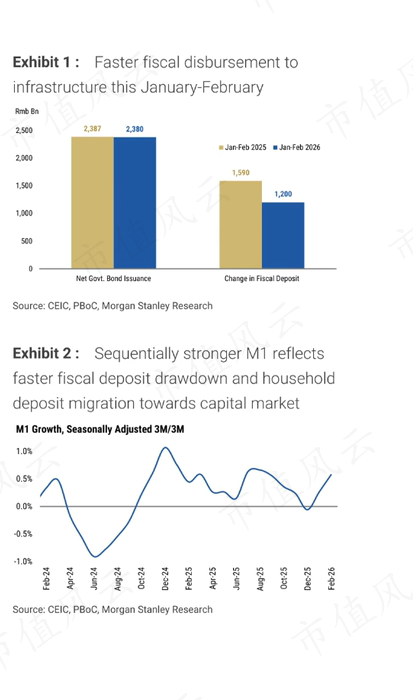

Fiscal disbursement to infrastructure likely accelerated, evident in:

Faster drawdown of fiscal deposits: January-February new fiscal deposits

this year were ~Rmb40Obn lower YoY, despite a similar scale of government

bond issuance, pointing to quicker deployment of funds.

Stronger long term corporate lending momentum: Seasonally adjusted

MoM growth in long term corporate loans rose 30bp to 0.7%, signaling

firmer infrastructure related borrowing.

Seasonally adjusted Mi YoY also rose for the second straight month - likely

reflecting the faster deployment of fiscal deposits in construction activity (a rise in

corporate demand deposits), as well as continued shift of household deposits

towards financial products (higher-than-seasonal NBFl deposits vs. lower-than

seasonal household deposits in January-February)

Outlook -front loaded infrastructure to anchor 1Q growth: The NPC kept the

augmented fiscal deficit target unchanged at 10.4% of GDP, but a faster public capex

cadence and prevailing export strength could keep 1Q real GDP growth at ~4.8%Y

But this momentum is unlikely to be sustained amid persistent consumption and

housing weakness; downside risks would rise if a prolonged oil shock triggers global

demand slowdown.

回复

回复