会员

会员 下载APP

下载APP

Despite exponential growth in 2025, Pop Mart's 4Q25 sales and

2026 guidance dampened bulls' conviction and lead us to cut

our 2026-27 earnings estimates ~4%.Overseas growth should

be slower in 2026, but we think the offline-driven growth model

continues to work.

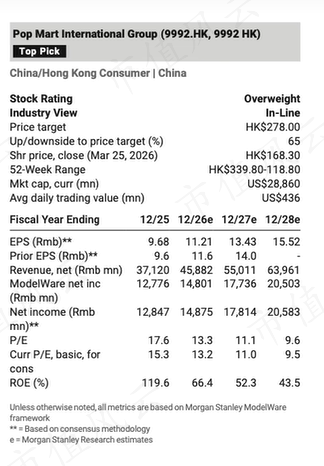

Stock view and estimates: Pop Mart's stock dropped 22% yesterday (vs. HSI +1%)

reflecting investor disappointment with 4Q25 sales growth (>120% y/y per MSe)

and 2026 sales guidance of >20%, as bulls looked for RMB16.5-17bn earnings for

2026 (see our prior note). Our estimates sat at the lower bound of consensus, and

after trimming our 2026-27 sales estimates by 4-5% and NP estimates by ~4%, we

now expect RMB45.9bn sales (up 24%) and RMB15.1bn non-IFRS NP (up 16%)in

2026.We also trim our target P/E from 26x to 23x to reflect slower overseas

growth. Together, this sees our price target fall ~14% to HK$278. But, we remain

Overweight. The stock is trading at 14x 2026 P/E (on MSe). We think that is

undervalued, as we believe it is still gaining share in a growing global lP collectibles

market, and the business adjustment efforts should make it more competitive in

2027-28.

We expect ~50% and 5-10% sales growth for 1H26 and 2H26, respectively. The weak

y/y growth in 2H26 is mainly due to the company's unprecedented pre-sale

measures for Labubu plush, aided by strong social-media tailwinds. On a sequential

basis, we expect 2Q/3Q26 to see sales growth acceleration q/q, which should lead

to a pickup in growth in 2027. The underlying drivers are store openings and new

product launches. Historically, the company's offline stores have been the largest

channel for new customer gains, except for 2025. For new stores, we assume 20 and

90 net openings for China and overseas in 2026, respectively. We also assume China

store productiyity rises and overseas store productivity falls in 2026 (we had baked

in these trends in our prior estimates).

回复

回复